Published last week (09 August) the provisional data shows that 774,964 tonnes of RDF was exported from England between January and June 2023, up from the 723,890 tonnes exported in the same period in 2022.

This reverses a period of declines in recent years as more domestic capacity ramps up. The same statistics last year, for the first half of 2022, showed a 10% year-on-year decline (see letsrecycle.com story).

The rise is thought to be partly down to reduced waste production in Europe and the need to reduce gas usage from Russia.

Countries

Sweden remains the top importer of waste from the UK, taking in 340,996 tonnes of RDF from England. This accounts for around 44% of the first half of the year.

The Netherlands remains a large importer too, despite a €31 per tonne tax placed on the import of waste back in 2020. The country took in 208,479 tonnes of waste from England, accounting for just under 27%. The other countries who import large amounts of English waste include Germany, Norway and Denmark.

In terms of companies, the largest exporter of RDF in the first half of 2023 was Geminor. The company exported 120,654 tonnes of RDF. This was followed by Andusia on 92,623, Probio on 90,298 and Bertling on 84,488.

Analysis

Andrew Gadd, company manager at environmental consultancy Footprint Services, said: “The data appears to indicate that the green shoots of recovery appear to be strengthening, for RDF exports at least. After several years of strong headwinds, it is pleasing to see so much positivity and renewed vitality in the market.”

Footprint Services also undertook a detailed analysis into the RDF data for the 12 months to June 2023.

For the 12 months to June 2023, the company explained that overall increase in RDF and SRF combined is +2%, with RDF up 15% year-on-year but SRF deceasing.

Mr Gadd added: “Behind the headlines, then, there are two distinct narratives at play between the RDF for municipal waste-to-energy plants, and SRF which are typically produced as an alternative fuel for the cement industry.

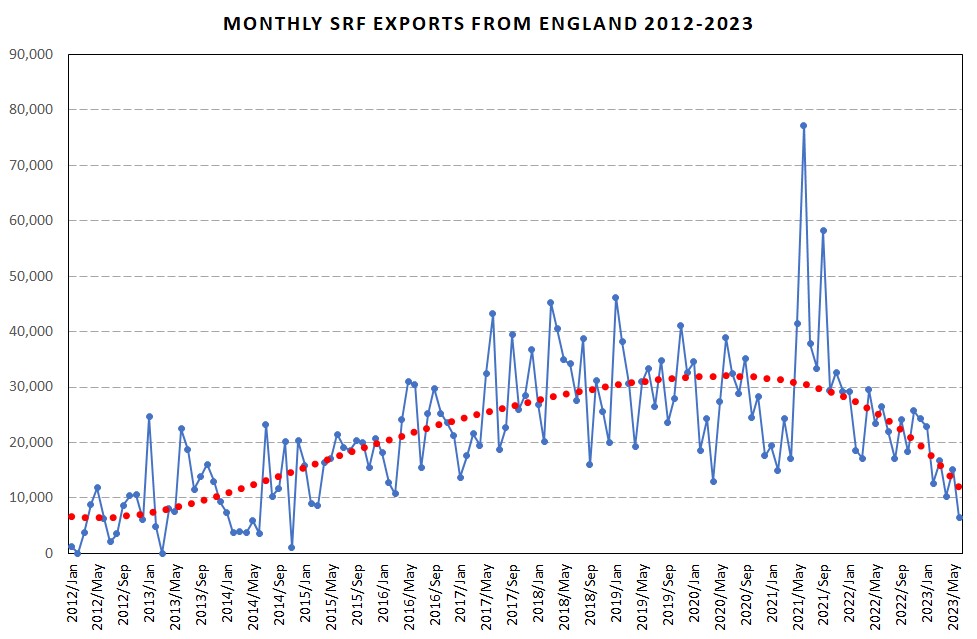

“The SRF story is markedly different, down by -41%. So, although the SRF fraction is much smaller than the RDF tonnage, the decline is still sufficient to drag down the headline numbers.”

Traditionally, SRF has had a wider geographic reach than RDF, extending to Eastern or Southern Europe, or even to more distant locations such as India, Morocco, Senegal, and the United States.

The added burden of elevated shipping costs for SRF to distant destinations, particularly given the soaring price of fuel, exacerbates the situation. Operators capable of flexibly transitioning between RDF and SRF production demonstrate greater resilience in such fluctuating environments.

Register for free to comment