PRN prices have been exceptionally high in recent months, with aluminium, the glass markets and plastic all comfortably above £100. Steel, paper and wood have also all between £25-£60.

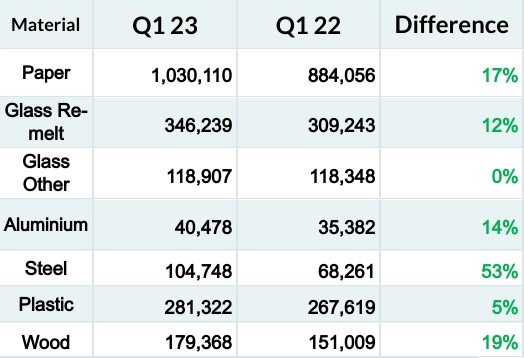

Published this week by the Environment Agency, the provisional data for the first quarter of 2023 (Jan-Mar) has shown that all materials are ahead of the same period in 2022.

Target

The first quarter data is usually compared with the same period the year before as targets for the compliance period are set in early May.

Many PRN traders have thus warned that the success of the Q1 figures can only truly be understood once this data is released.

Targets are set as a percentage of what is placed on the market in the previous year, so could be lower if the cost-of-living crisis meant there was less packaging bought.

Prices have already started correcting

- Tom Rickerby, t2e

Price movements

Tom Rickerby, head of trading at the Environment Exchange (t2e) PRN trading platform, explained that the data has meant that many prices are starting to come down, going so far as to say the “bubble is bursting” in the market.

He explained: “The bubble appears to be bursting for the recent PRN bull market. The release of strong Q1 supply data has sellers now nervously looking to the downside.

“Prices have already started correcting on t2e with the paper market seeing the heaviest loses, collapsing 48% on its pre-data price to £17.00 per tonne. Steel and wood have seen a continuation of the downward trend established earlier in the quarter, whilst glass and aluminium have all come off year highs this week, reversing their 3 month inflationary price trend. Glass remelt fell 12% to £125, whilst glass other lost a quarter of its value, dropping to £100 per tonne.

“Surprisingly, despite being the only material that looks to have underperformed in the period, plastic has also been caught up in the general market sell off, falling 5% to £295.”

Mr Rickerby added that all eyes will now be on the obligation data release in May, where a widely anticipated fall in 2023 demand may inflict “further short-term damage” to PRN prices.

There’s potential for a slightly more steady market

- Martin Trigg-Knight, Clarity Environmental

‘Recovery’

With less packaging on the market in 2022 due to falling waste volumes, with targets set on waste levels in 2021, last year was a difficult time in the markets.

While all material targets were met, the amount of carry-over PRNs into the year saw a huge decline, down around 75% to levels not seen since 2008.

While it was feared the lack carry-over would spook the market in 2023, Martin Trigg-Knight, director of compliance services at Clarity Environmental and chair of the Packaging Scheme Forum, said the Q1 Data “shows a steady recovery”.

He explained: “Paper in particular has recovered well, showing that a large amount of PRN tonnage was previously missing from the voluntarily monthly data reported in the early part of this year. Already the paper price has responded to the increased availability showing the responsiveness of the PRN system to times where less recycling subsidy is needed.

“Both glass and plastic are currently showing behind initially expected target volumes at Q1, but early indications of UK producer obligations show that there is potential for glass and plastic obligations to reduce this, so whilst right now these commodities look short, context might later show that availability is better. If this is the case then there’s potential for a slightly more steady market in the early part of 2023.”

‘Two halves’

Paul van Danzig, policy director at the Wastepack Group said the numbers show “a tale of two halves”.

He said while paper and wood have shown positive progress, “it’s the usual suspects that cloud the picture”.

Mr van Danzig explained: “Plastic for example is up on this time last year – which is good, but if you extrapolate the numbers and add the small amount of carry in – then the numbers are once again going to be tight against the perceived obligations this year – I guess the key to everything will be the UK obligations for 2023. Once we see this data we’ll really know how well or how bad these interim numbers actually look like – I guess all eyes will be on early May which is usually when the Environment Agency publish the UK obligations.”

System

David Daw, projects analyst at Valpak, explained that the high paper and aluminium volumes have offset what was a slow start to the year with the historically low carry forward.

Mr Daw said: “The positive Q1 volumes highlight the robustness of the PRN system in adapting to challenges and support the recycling process. This has been aided by an increased number of reprocessors getting accredited compared to 2022. The strong Q1 figures, coupled with the expected decrease in obligation for 2023 which will be published in mid-May, should take some of the pressure out of the PRN market. With confirmation of the delay of the Scottish DRS, the PRN market can operate with a greater degree of certainty throughout the remainder of the year.”

He added that a factor which could impact the PRN market for the remainder of the year is the likely lower waste arisings across all materials due to the cost-of-living crisis. If sustained throughout the year, Mr Daw said, this could reduce the volume of PRNs generated and then in turn lead to price rises in order to meet the UK targets.

“It is still early in the year and the Q1 figures should be treated with positive caution,” he concluded.

Subscribe for free