The provisional data for the second quarter of the year (April-June) was published earlier this week on the National Packaging Waste Database.

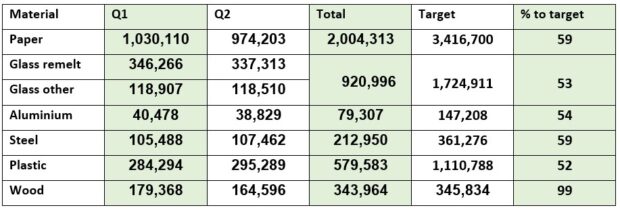

As outlined below, it shows that all materials are at least 50% towards their obligations at the halfway point of the year, before carry over is also included. However, the data is provisional and subject to change.

Compliance specialists have all warned however that the obligation is also likely to rise later in the year, as more producers submit figures from 2022. Targets are based on a percentage of material placed on the market the previous calendar year.

‘Nerves’

The data release has been welcomed by the compliance sector, but some warnings have been sounded too.

Andrew Letham, operations manager at The Environment Exchange, told letsrecycle.com that Q2 data was positive for most materials’ growth, but he said the growth from the monthly optional data was “slightly lower than expected and nerves will remain in a few materials”.

He explained: “Paper/General Recycling currently looks comfortable with prices dropping 30% from the release of the monthly data to £7. Plastic on the other hand looks to be just scraping by with the 295,000 tonnes reported as recycled in Q2 not as large as anticipated and prices settling at £270 after a 10% drop prior to the data. ”

He also noted that that much will depend on the growth in obligation between now and the end of the year as well as the material markets ability to keep producing large PRN returns against a slowdown in demand for finished product and softening PRN prices.

‘Easing concerns’

Martin Trigg-Knight, director of compliance services at Clarity Environmental, said the data will go some way to easing early concerns about the production of glass, which he explained has been “eased by solid production of the last few months.

Mr Trigg-Knight added: “Normally with high interest rates, and cost of living difficulties, the public consumes less bottled alcoholic beverage, and although wine sales are reduced, it seems that other glass use must be compensating, as Glass Remelt figures are good.

“This data also seems supported by lower obligation volumes in currently available data both in Glass and Plastic. As a result the market seems to be stabilising; however, caution is urged as the currently available obligation data is still incomplete, and the PRN volume requirement for 2023 will increase as more late producers submit their data over the next few months.”

‘Promising’

David Daw, projects analyst at Valpak, explained that the figures are “promising” in comparison to the same quarter in 2022, when targets were much tighter (see letsrecycle.com story).

However, he also noted fears that the obligations could rise in the future.

He added: “The tight market and the PRN prices experienced over the last couple of years have contributed to investment in reprocessing and a significantly higher number of reprocessors and exporters have become accredited this year compared to 2022.

” As long as the recycling markets remain operating smoothly we should see prices for the majority of materials continue to ease down in the second half of the year. Although the impact of cost-of-living concerns are impacting on the amount of waste arising and hence material available for recycling. Valpak is monitoring the situation closely.”

We recognise that the supply chain for glass aggregate and plastic recycling still requires strong support

- Sandeep Attwel, Envirovert

Prices

Sandeep Attwel, commercial director of Envirovert, predicted that the data will lead to some “immediate softening of prices” in most markets as the figures show targets are on track.

However, said said while “significant progress” has been made, “It’s important to acknowledge the materials that are facing supply challenges”.

Ms Attwel said: “We recognise that the supply chain for glass aggregate and plastic recycling still requires strong support. Glass aggregate is less of a risk due to the over supply in glass remelt, however plastic remains a challenge and price softening will not be helping the supply chain as we go into Q3.

“One aspect that presents a moving target in our recycling journey is the demand. As we analyse market trends and consumer behaviour in 2022, we understand that demand might not reach the same heights as in previous years. A lower demand may just help ease the supply pressures in the market for materials that need further support.”

Subscribe for free